Skip to content

Skip to content Home renovations are an excellent way to improve your living space, increase functionality, and add value to your property. However, before starting, it’s essential to understand how much you can afford. A Home Equity Line of Credit (HELOC) or home equity loan is a popular way to fund renovations, but you need to calculate your home equity first. This guide will break it down with simple explanations, examples, and actionable steps—tailored for Oregon homeowners.

If you are looking for a more in-depth and personal discussion with our team regarding your specific project, feel free to book a hassle free, no obligation 1 on 1 virtual consultation with our Construction Consultant:Book a Call.

What Is Home Equity?

Think of your home’s equity like the “owned” portion of your house. If your home were a pie, your equity is the slice you’ve paid off through your mortgage or upfront payments, while the rest of the pie is owned by the bank.

Simple Formula for Home Equity:

Example:

- Your home’s current market value is $600,000.

- Your remaining mortgage balance is $350,000.

Calculation: You have $250,000 in home equity.

Steps to Calculate Your Home Equity

1. Determine Your Home’s Current Market Value

Your home’s value can fluctuate over time due to market conditions. To find the most accurate estimate:

- Hire a Professional Appraiser: This is the most reliable method, especially if you’re preparing for a HELOC application.

- Use Online Tools: Websites like Zillow or Redfin offer quick estimates based on recent sales in your area.

- Check Recent Sales: Look at comparable homes sold recently in your Oregon neighborhood.

2. Find Your Remaining Mortgage Balance

This is the amount you still owe on your home loan. You can find this information on your latest mortgage statement or by contacting your lender.

Example:

- Mortgage balance: $350,000

- Market value: $600,000

Your home equity is $250,000.

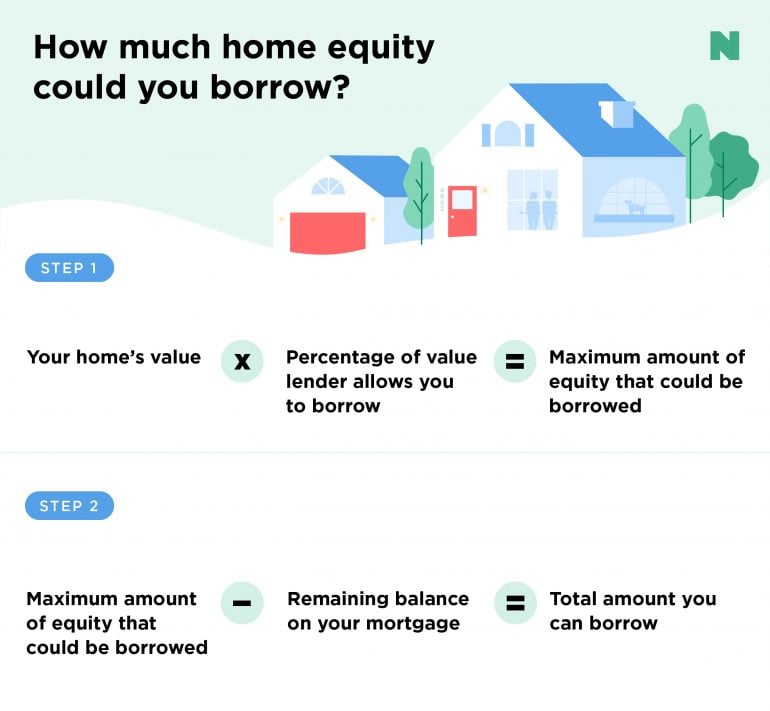

3. Calculate Borrowable Equity

Most lenders allow you to borrow up to 80-85% of your home’s total value, including your current mortgage balance. This percentage is known as the combined loan-to-value (CLTV) ratio.

Formula:

Example:

- Market value: $600,000

- CLTV limit: 85% (0.85)

- Mortgage balance: $350,000

Calculation: You could borrow up to $160,000.

Why Use Home Equity for Renovations?

A HELOC or home equity loan offers unique benefits:

- Lower Interest Rates: These loans typically have lower rates than personal loans or credit cards because they’re secured by your home.

- Flexibility: Borrow only what you need with a HELOC or opt for a fixed loan amount with a home equity loan.

- Tax Benefits: Interest paid on a HELOC used for home improvements may be tax-deductible (IRS).

Simple Analogy:

Think of your HELOC as a credit card backed by your home. You can “charge” renovation costs up to your approved limit and pay interest only on the amount you use.

Examples of Renovations and Equity Usage

Example 1: Kitchen Remodel

- Cost: $50,000

- Borrowable Equity: $160,000 (as calculated above)

- Plan: Use $50,000 from a HELOC to fund high-quality materials and appliances.

Example 2: Adding an ADU

- Cost: $100,000

- Value Added: ADUs in Oregon can increase property value by $150,000 and generate $1,800/month in rental income (Oregon Housing Bureau).

How the Oregon Preconstruction Process Helps

The Oregon Preconstruction Process ensures that your home equity is used effectively for maximum impact. Here’s how:

1. Strategic Budget Planning

Identify high-ROI projects, like kitchen remodels or energy-efficient upgrades, to prioritize your renovation dollars.

2. Detailed Design Planning

Collaborate with architects and contractors to finalize designs that align with your budget and goals.

3. Timeline Management

Ensure HELOC funds are available at each renovation milestone, avoiding delays.

Case Study:

A Laurelhurst homeowner used a $75,000 HELOC through the Portland Preconstruction Process to remodel their kitchen and add solar panels. The upgrades increased the home’s value by $125,000 and reduced energy bills by $2,000 annually.

Potential Risks and How to Mitigate Them

Risk 1: Over-Borrowing

If you borrow too much and housing prices drop, you could owe more than your home is worth (negative equity).

- Solution: Borrow only what you need and prioritize high-value renovations.

Risk 2: Variable Interest Rates

HELOCs often have variable rates, which can increase over time.

- Solution: Consider a fixed-rate HELOC if you prefer payment stability.

Risk 3: Mismanagement of Funds

Without a clear renovation plan, costs can spiral out of control.

- Solution: Work with professionals through the Oregon Preconstruction Process to stay on budget.

Final Thoughts

Calculating your home equity is the first step in budgeting for a renovation. By understanding how much equity you have and working with tools like the Oregon Preconstruction Process, you can plan a successful renovation that adds value and functionality to your home. Whether you’re upgrading your kitchen, adding an ADU, or improving energy efficiency, leveraging your home’s equity is a smart, cost-effective choice.

Ready to transform your home? Contact Harris & Sons today to learn how we can help you maximize your equity and create your dream space. Get in touch and explore our services.